*These funds use the PVC LargeCap S&P 500 Managed Volatility Index Account

Principal® Lifetime Income Solutions II

Guarantees are better than hope

Markets go up and down, so losing investment value is a reality for most of us. But it’s harder to deal with in retirement. And without a source of guaranteed income, this could affect how much your clients can spend.

Providing a source of guaranteed income, like that provided by Principal Lifetime Income Solutions II Variable Annuity (PLIS II), can help insure you won’t have to do that.

Ready to get started?

Fill out our form for more information, and we'll be in touch as soon as possible.

The benefits of PLIS II

PLIS II may allow your client to keep pace with inflation by keeping money invested in the market. They enjoy tax-deferred growth potential and can access money through scheduled and unscheduled withdrawals. Plus, PLIS II offers a guaranteed death benefit, so clients can leave a financial legacy to their loved ones.

Guaranteed income riders

Three guaranteed minimum withdrawal benefit (GMWB) riders are available—Target Income Protector, Flexible Income Protector, and Flexible Income Protector Plus. Your clients can choose the rider that best fits their financial goals. Each creates a guaranteed income stream they can’t outlive.1

Bonus and step-up features

PLIS II’s annual step-up feature is available with each of the three GMWB riders. Annual market gains are locked into a client’s withdrawal benefit base.2 The annual bonus is available with the Target Income Protector and Flexible Income Protector Plus riders.

Both of these features are provided at no extra cost and offer another way to way to increase your clients' future guaranteed income.

Investment options

Your clients will be able to allocate money to a number of different subaccount investments depending on the rider they choose. Our riders are designed to offer both traditional and risk-controlled funds. The right one for your clients depends on how much risk they’re willing to take with their investment.

Target Income Protector

- Diversified Growth Volatility Control*

- Diversified Balanced Volatility Control*

- Diversified Income

- Fidelity VIP Government Money Market

- 6- & 12-month DCA accounts

Flexible Income Protector

- Diversified Growth

- Diversified Balanced

- Diversified Income

- Diversified Growth Managed Volatility*

- Diversified Balanced Managed Volatility*

- Fidelity VIP Government Money Market

- 6- & 12-month DCA accounts

Flexible Income Protector Plus

- U.S. LargeCap Buffer July

- Diversified Income

- Fidelity VIP Government Money Market

- 6- & 12-month DCA accounts

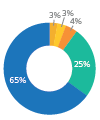

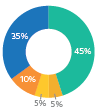

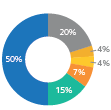

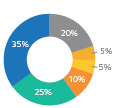

Investment asset allocation

PVC Bond

Market

Index Fund

PVC Large

Cap S&P 500

Index

Account

PFI MidCap

S&P 400

Index Fund

PFI SmallCap

S&P 600

Index Fund

PFI

International

Equity Index

Fund

Volatility

Control

Overlay

Traditional diversified funds

These are composed of indexed funds that utilize a lower cost fund of funds investment strategy. They have a pre-determined allocation that are rebalanced monthly to the original allocation. Traditional diversified funds are designed to be cost effective and easy to understand investment options.

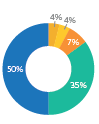

Diversified

Income

35% equity

65% fixed income

Diversified

Balanced

50% equity

50% fixed income

Diversified

Growth

65% equity

35% fixed income

Managed volatility diversified funds

These funds seek to act as a shock absorber during periods of high market volatility. They are sub-advised by Spectrum Asset Management using a proprietary method to predict and manage market volatility. Managed volatility diversified funds employ some active management techniques.

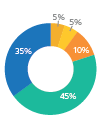

Diversified Balanced

Managed Volatility*

50% equity

50% fixed income

Diversified Growth

Managed Volatility*

65% equity

35% fixed income

Volatility control diversified funds

These funds are sub-advised by Principal Global Equities and use a pre-determined rules-based approach to react to market volatility. Volatility control diversified funds utilize a 100% reactive strategy

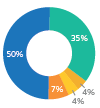

Diversified Balanced

Managed Control

50% equity

50% fixed income

Diversified Growth

Volatility Control

65% equity

35% fixed income

Additional volatility protection

Our riders are designed to offer both traditional and risk-controlled funds. Risk-controlled funds use investment strategies designed to offer protection from the ups and downs of the market. Ours are based on our traditional Diversified funds. They don’t eliminate risk for losses but seek to manage equity exposure based on market volatility.

PLIS II resources

Investment

performance

The importance

of guarantees

Explaining a guaranteed

income floor to clients

1 While it's necessary to select one of these riders with the annuity contract, clients can choose to cancel it after the fifth year of the contract.

2 Available until age 80 or until client has been in the contract for ten years, whichever comes later.

Withdrawals prior to age 59½ are subject to a 10% IRS penalty tax.

For financial professional use only. Not for distribution to the public.

Tax-qualified retirement arrangements, such as IRAs, SEPs and SIMPLE-IRAs are tax deferred. You derive no additional benefit from the tax-deferral feature of the annuity. Consequently, an annuity should be used to fund an IRA, or other tax-qualified retirement arrangement, to benefit from the annuity's features other than tax deferral. These features may include guaranteed lifetime income, death benefits without surrender charges, guaranteed caps on fees and the ability to transfer among investment options without sales or withdrawal charges.

Annuity products and services are offered through Principal Life Insurance Company. Principal Variable Contracts Funds are distributed by Principal Funds Distributor, Inc. Securities offered through Principal Securities, Inc., member SIPC, and/or independent broker/dealers. Referenced companies are members of the Principal Financial Group®, Des Moines, Iowa 50392, principal.com.

Guarantees are based on the claims-paying ability of the issuing insurance company.

All guarantees and benefits of the insurance policy are backed by the claims-paying ability of the issuing insurance company. Policy guarantees and benefits are not obligations of, nor backed by, the broker/dealer and/or insurance agency selling the policy, nor by any of their affiliates, and none of them makes any representations or guarantees regarding the claims-paying ability of the issuing insurance company.

Contract rider descriptions are not intended to cover all restrictions, conditions or limitations. Refer to rider for full details.

Principal®, Principal Financial Group®, and Principal and the logomark design are registered trademarks of Principal Financial Services, Inc., a Principal Financial Group company, in the United States and are trademarks and service marks of Principal Financial Services, Inc., in various countries around the world.

2874476-052023